• Oil markets are currently governed by low oil prices, high interest rates and a subdued growth outlook, not by regulatory barriers to new drilling.

• US producers have learned discipline over the last few years and are unlikely to shift their focus from stability and cash flows toward growth and capital expenditures (CapEx) without more permanent legislature.

• Price trends over the next few years will be driven by macroeconomic fundamentals (such as economic growth, the strength of the dollar, sanctions and geopolitical tensions) rather than a sudden surge in US production.

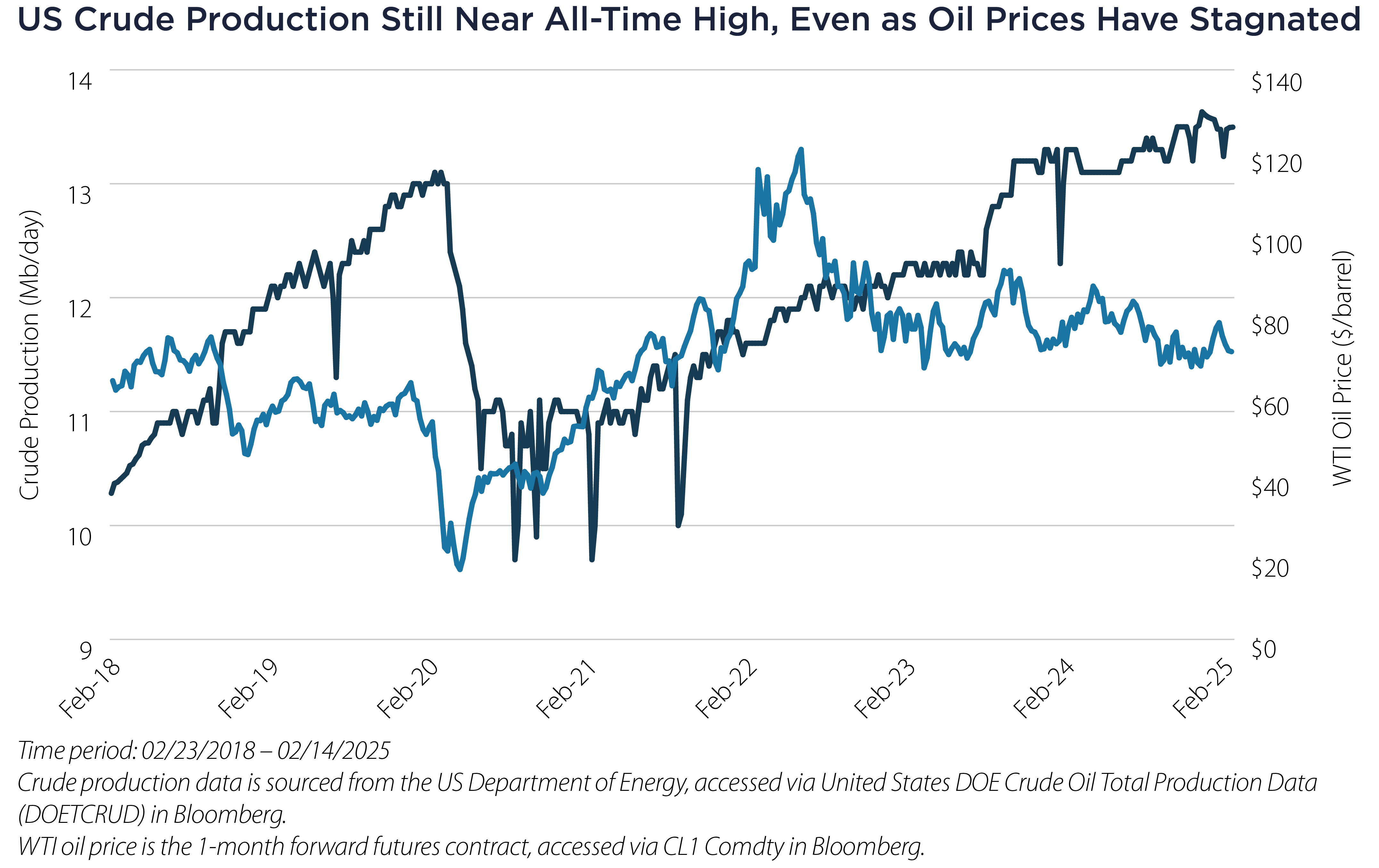

Popular rhetoric from the new US administration suggests that easing regulations and accelerating drilling permits would unleash a US oil production boom. A closer look at production dynamics reveals that this narrative overlooks several key realities. Rather than being bottlenecked by permitting processes, US oil producers are already producing at record levels. In fact, new drilling is currently more constrained by low oil prices, high interest rates and an uncertain future than by regulatory hurdles.

ExxonMobil CEO Darren Woods expressed skepticism in November that a more “oil‐friendly” administration could substantially increase output simply by speeding up permit approvals, noting that production decisions are fundamentally governed by economic factors. “I don’t think US production is constrained, so I don’t know that there’s an opportunity to unleash a lot of production in the near term…” said Woods in an interview with Semafor at the 2024 United Nations Climate Change Conference (COP29).1

Low oil prices are the main determinant of oil production profitability, and the International Energy Agency (IEA) and the US Energy Information Administration (EIA) both anticipate supply growth—primarily stemming from ex-OPEC+ producers—outpacing demand over the next couple years.2,3 This sort of environment is not one in which producers will be keen to make additional, unplanned investments in expansions that would only push prices lower.

New oil field development in Alaska, the focus of a recent executive order, is relatively time- and capital-intensive when compared to drilling in established fields in regions such as the Permian Basin, where new wells can be brought online in just a couple months.4,5 This means high capital costs, due to current interest rates, and an uncertain political climate, due to the impermanence of executive orders, are further barriers to large-scale developments in Alaska.

Given the rapid pace of news, it’s important to stay grounded in the fundamentals of what really drives changes in commodity markets. The shareholders of US producers have come to expect stability and high cash flows instead of growth and CapEx. The main drivers of oil prices over the coming years are therefore likely to be economic growth, the strength of the dollar, sanctions on oil producers and geopolitical tensions, not a rapid expansion of US production.

Important Disclosures & Definitions

1 Matthews, C. (November 12, 2024). Exxon CEO says Trump won’t be able to “unleash” new energy production. MarketWatch.

2 US Energy Information Administration (EIA). (2025). Short-Term Energy Outlook – February 2025. US EIA.

3 International Energy Agency (IEA). (2025). Oil Market Report - February 2025. IEA, Paris.

4 Dang, S., & Volcovici, V. (January 23, 2025). Oil industry unlikely to rush to Alaska despite Trump’s call to drill. Reuters.

5 Stanford University. (October 2024). Drilling, completing, and producing from oil and natural gas wells. Stanford Doerr School of Sustainability, Understand Energy Learning Hub.

AAI000891 02/25/2026